Greetings and Happy Friday!

Trusting you’re looking forward to a good weekend! Just a note to let you know that our office will be closed on Monday with Tuesday being Freedom Day.

To continue from last week’s theme of global trends, this week we can see how our lives have been affected by technology, which has also been fast-tracked by the epidemic. Those of us who are basically or wholly financially independent have actually seen our investment portfolios improve and have, while being confined to home, stayed connected by dramatically-improved digital communication systems and media. At the same time, we’ve been able to use technology to do our shopping virtually with the convenience of delivery to our doors.

Online life has been radically fast-tracked by Covid-19 precautions and a lot of the way we do things now will not change back to the “old” days. While the world scrambles to adapt to what’s going on while trying to figure out what to believe or not, we need to be flexible about change and try to assimilate the the best of these new ways to adapt and improve our lives as well as those of others.

5 Big Picture Trends Being Accelerated by the Pandemic

From Visual Capitalist

As every email introduction has reminded us in 2020, we’re living in “unprecedented times”.

No doubt, even after a viable vaccine is released to the general public and things begin to return to some semblance of normalcy, there will be long lasting effects on society and the economy. It’s been said that COVID-19 has hit fast forward on a number of trends, from e-commerce to workplace culture.

Today, we’ll highlight five of these accelerating trends.

The following article uses charts and data from our new book Signals (hardcover, ebook) which covers the 27 macro trends transforming the global economy and markets. In some cases, where appropriate, we’ve added in the most recent projections and data.

#1: Screen Life Takes Hold

Smartphones have drastically altered many parts our lives – including how we spend time. In the decade from 2008 to 2018, screen time on mobile devices increased 12x.

Fast forward to today, and screen time is up across the board, with some of the most dramatic increases seen among kids and teenagers. 44% of people under the age of 18 now report four hours or more of screen time per day – up from 21% prior to the pandemic.

Gaming is another digital segment that has benefited from the pandemic. Video game revenue spiked in the springtime, and sales have remained strong going further into 2020. Companies are hoping that casual gamers won over during lockdown will continue playing once the pandemic has come to an end.

Acceleration signal: International bandwidth and internet traffic was already increasing steadily, but COVID-19 stay-at-home activity has blown away previous numbers.

Even as more workplaces and schools begin to operate normally again, it’s doubtful that screen time will drop back down to pre-COVID levels.

#2: The Big Consumer Shake-Up

The consumer economy has been innovating on two fronts: making physical buying as “frictionless” as possible, and making e-commerce as nimble as possible. COVID-19 broke old habits and sped up that evolution.

Innovations in real world shopping appear to be moving in the direction of cashierless checkouts, but in order for that model to work, people first need to embrace contactless payment methods such as mobile wallets and cards with tap payment.

So far, the pandemic has been an accelerant in moving people away from cash and pin-and-swipe credit cards in lagging markets. Once people get used to the convenience of contactless payments, it’s likely they’ll continue using those methods.

Of course, no conversation about e-commerce is complete without talking about Amazon. The company has seen consistent growth in subscription revenue in recent years, and the company’s actions have a wide-reaching effect on the rest of the industry.

Much like the gaming industry, e-commerce companies like Amazon are hoping that people who dabbled with online ordering during the pandemic months, will convert into lifelong customers.

Acceleration signal: E-commerce penetration projections have shifted upward.

In hindsight, 2020 could be an inflection point where e-commerce gained a much bigger slice of the overall retail pie.

#3: Peak Globalization

Globalization went on a tear starting from the mid-1980s until it hit a plateau during the financial crisis. Since that point, global trade as a percentage of GDP has flat-lined in the face of trade wars, and now COVID-19.

Trade was obviously impacted by the pandemic, and it’s too early to say what the long-term effects will be. One thing that is clear is that the information component of globalization is becoming an even more important piece of the world’s economic puzzle.

Even before COVID-19 took hold, the global services trade was growing 60% faster than the goods trade, and was valued at approximately $13.4 trillion in 2019.

Acceleration signal: The dip in merchandise trade looks eerily similar to the one that took place in 2008.

#4: The Wealth Chasm

On the high end of the wealth spectrum, billionaires are worth more than ever.

Meanwhile, in the broader economy, inequality has grown over the last few decades. Those in the top 50% wealth bracket have seen increasing gains, while the bottom 50% have seen stagnation.

This issue is sure to be compounded by economic turmoil brought on by COVID-19. Younger generations face the dual challenges of being more likely to be negatively impacted by the pandemic, while also being the least likely to have savings to cover an interruption in income.

In fact, nearly half of people in the 18–24 year old age group have nothing saved at all.

The longer the economy is affected by COVID-19 measures, the more of a wedge will be driven between people who have continued working and those who are employed in impacted industries (e.g. tourism, events).

Acceleration signal: Growth in the net worth of billionaires has been largely unaffected by COVID-19.

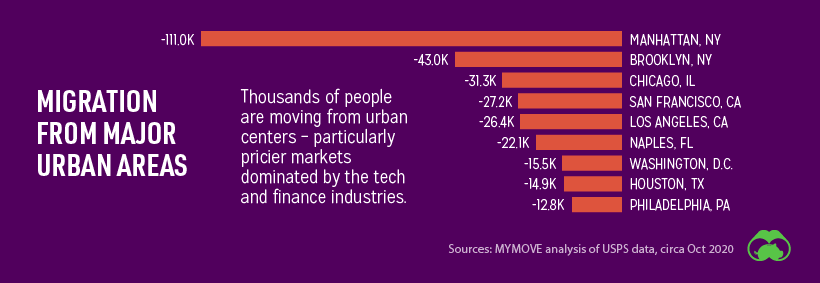

#5: The Flexible Workplace

As of 2019, over half of companies that didn’t have a flexible or remote workplace policy cited “longstanding company policy” as the reason. In other words, that is just the way things have always worked.

Of course, the pandemic has forced many companies to rethink these policies.

This grand experiment in remote work and distributed teams will have an impact on office life as we know it, potentially reshaping the entire “office economy”. The impact is already being felt, with global commercial property investment volume falling by 48% in Q3 2020.

Acceleration signal: Thousands of people are moving out of pricey urban areas, presumably because they are able to work remotely from a cheaper location.

In the News this Week:

Friday, 23 April 2021

The US markets closed lower after reports that President Biden is considering nearly doubling capital gains taxes on the wealthy. All 11 sectors of the S&P500 closed lower, tech some of the biggest losers as Micron, Twitter and Western Digital all lost more than 4%. Blackstone group shares climbed 2.65% after the Private Equity group reported a record 1st quarter profit. Intel fell 2% in after-hours trade on lower sales and revenue report. PMI and New home sales key numbers to watch today. Ping an, Honeywell, Daimler and American Express to report earnings today. The US 10-year treasury yield moved down to 1.554%.

European equity indexes finished higher. European food and beverage stocks, technology and utilities were the best performers. Financial services, telecom and insurance lagged. As expected, the European Central Bank left key policy settings and guidance unchanged. The statement reiterated it expects asset purchases to continue to be conducted at a significantly higher pace compared to the start of the year.

S&P500 -0.92% Dow -0.94% Nasdaq -0.94% FTSE100 +0.62% DAX +0.82% CAC +0.91%.

Asian equities mixed this morning. The Hang Seng outperforming early as mainland China opens flat. Nikkei lagging. Japan reported a flash PMI that is the highest in 3 years while their inflation declined in March.

Nikkei -0.85% Hang-Seng +0.87% Shanghai +0.05% ASX -0.13%

The JSE All-Share index closed lower after Resources pulled back as commodity prices took a breather after the recent rally. Precious metals fell 1.9% pulling the Resource sector lower by 0.91%. Altron jumped 5.68% after confirming a special dividend of 96 cents per share. The 10-year Government bond closed weaker at 9.125%. Harmony is set to release results today.

Notable Gainers/Losers

Pepkor +4.83% ARM +3.17% Santan +2.93% Bidcorp +1.92% Prosus +1.65% AB Inbev +1.53%

Northam -3.44% Implats -3.09% MTN -2.81% Sibanye -2.66% Ninety1 -2.19% Sirius -2.12%

JSE All-Share -0.26% JSE Top 40 -0.35% Industrials +0.08% Resources -0.91% Financials -0.26%

JSE All-Share 66’972

S&P500 4’135

USDZAR 14.30

EURZAR 17.20

GBPZAR 19.82

EURUSD 1.20

GBPUSD 1.39

GBPEUR 1.15

AUDZAR 11.05

NZDZAR 10.26

Brent Crude $65.70

Gold $1’787

Platinum $1’206

Palladium $2’837

Sources: Factset, Yahoo Finance, Trading Economics, BusinessDay Live, WSJ

Please give us a call or email if you need any assistance. Have a great weekend!

Kind regards,

Your TurnPoint Team

Vic Hodoul CFP®

Certified Financial Planner®

Cell +27 (0) 79 353 1076

Email vic@turnpoint.co.za

Office/Admin Manager:

Arlene Schoeman: +27 (0)21 555 1010

Email arlene@turnpoint.co.za

TurnPoint Investments

Website: Authorised Financial Services Provider (FSP12820) (turnpoint.co.za)

Milnerton Office: 5 Royal Atlantic, Sunset Beach 7441

Cape Town Office: Suite 824, The Onyx, 57 Heerengracht Street, Foreshore 8005

Tel +27 (0)21 555 1010 Fax +27 (0)86 589 2738

Individual and Corporate Investment, Retirement, Estate, Risk and Tax Planning Solutions

TurnPoint Investments (Pty) Ltd. Registration Number 2003/020010/07 | Financial Service Provider (FSP licence number 12820) Directors VD Hodoul DL Hodoul